Critical Competition I: America’s Missing Middle

Accessing critical minerals is paramount for national security, defense, and energy-related applications. For the U.S. to truly reduce its dependency on Chinese-sourced minerals, the Trump Administration needs to focus on deposits as well as processing and refining capacity.

The recent interest in acquiring Greenland’s critical minerals spurred much-needed debate over how the U.S. can secure its supply chains, thereby reducing our dependency on Chinese-sourced materials. Javier Blas pointed out last week that while Greenland may have critical minerals such as REEs, the logistics of standing up a mine north of the Arctic Circle may be untenable from both logistical and economic standpoints. To add to that, global mining companies are facing historically low valuations, reducing their ability to raise capital at a reasonable cost, and increasing IRR hurdles. Greenland may be an untapped source of critical minerals, but access to these inputs for defense and renewable technology is not the crux of the issue, in my view. Mineral processing is the key and missing lynchpin of the West’s squabble to secure its supply chains.

China’s Midstream Dominance

China’s mineral processing dominance is not accidental, it’s a key feature of the CCP’s industrial overcapacity. Refining minerals into metals is capital, energy, and emission-intensive. Further, China’s vast state-subsidized vertical integration from its ownership of mines, and processing capacity of most of the world’s minerals, to manufacturing of final goods such as rare earth magnets and EVs is the reason why it can defend its market dominance. Refineries, for instance, operate on thin margins and charge based on market demand for metals, yielding around 5% profit margins. That’s a paltry margin for a standalone facility that can cost in the hundreds of millions or even billions and is often an ancillary part of a business. Moreover, refineries require economies of scale, the sine qua non to China’s global mineral dominion.

Importantly, critical minerals are heterogeneously distributed around the world (except for REEs), while refining capacity is not. Data from the IEA shows the extent to which China dominates mineral processing. Nearly all the world’s graphite is processed in China, while 75% of the world’s cobalt, 70% of lithium, and around a quarter of the nickel are processed on the mainland. Evidently, most of the world’s EV capacity and rare earth magnet is also produced in China too.

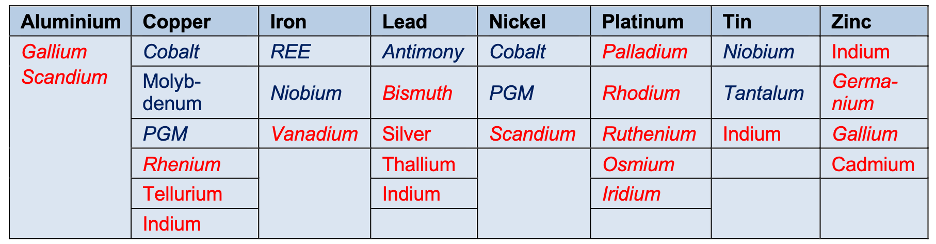

Another key point is that many of the world’s key materials such as gallium, germanium, and rhenium are not produced as primary products. Instead, they are by-products. Gallium, for instance, is extracted from the process of making bauxite into aluminum, germanium can come from the smelting of zinc, while rhenium is extracted via the process of refining copper. On their own, these metals don’t make the economics of mines work, so they are always extracted alongside other minerals. This is the key reason why China dominates the supply of minor metals.[1]

Greenland: The Penultimate Frontier

Enter Greenland, whose geology hints at deposits of REEs, graphite, PGMs, gallium, and germanium. Accessing Greenland’s minerals on their own will not cure America’s reliance on China unless it develops a network of domestic and international refining capacity. As it stands, even MP Materials—the U.S.’ only operating REE company—still ships its NdPr concentrate to China for refining. In the unlikely case that Greenland becomes a U.S. Territory, the Jones Act would get in the way of bringing concentrate back to the lower 50 states.

Humoring the idea that Greenland could be a viable source of minerals, there is some promise. Greenland may have 150,000t worth of Ga located in the Skaergaard Intrusion (assuming the entire zone of the Au-Pd deposit is mineralized) with around concentrations of 81-117ppm. As I noted before, gallium on its own is not economical and would need to be extracted alongside the PGMs and Au located in situ. Looking at other minerals Greenland deposits are varied, but few have a high probability of becoming a viable resource. Graphite, molybdenum, PGMs, tantalum, and zirconium seem to have potential. The reality is, however, that the disparity amongst deposits and small market sizes for many minerals from gallium to tantalum makes the thought of scaling up Greenland’s mining industry a daunting task. Perhaps Kobold could send an exploration team given its success in Zambia’s copper belt. Even assuming a significant discovery across a few key minerals and if all goes well, scaling up a mine then requires infrastructure for transport only to ship off concentrate, which the U.S. can’t refine, yet.

Aluminum Refining in the 20th Century

“By 1950, five aluminum smelters in the Pacific Northwest produced about 44% of all U.S. aluminum. Only 10 years earlier, not a pound of aluminum was being produced west of the Mississippi River. The speed and the magnitude of this development were mostly attributable to wartime demands.”[2]

The U.S. does have a history of standing up refining capacity, so long as the political will and determination are backed by capital. During the buildup of WWII, the government backed the development of America’s aluminum industry in the energy-rich Pacific Northwest. Evidently, the conditions that led to the buildup of America’s aluminum industry were predicated on war, but it nevertheless demonstrates what is possible with the spirit of capitalism.

Make By-Product Processing Great Again

Competing with China’s excess capacity in any regard isn’t a good idea, the CCP’s firms have little regard for profits nor free markets. The U.S. can, however, diversify critical mineral supply chains with a targeted focus on its midstream capacity. The example of aluminum is illustrative from an industrial policy standpoint on its own right, but it is also demonstrative of how the U.S. can take a step toward solving its supply chain vulnerabilities. Gallium, as I mentioned earlier, is a by-product of aluminum refining as it journeys to its final form. In fact, most of the U.S. problems related to critical minerals are by-products. Germanium, for instance, is a by-product of zinc, while rhenium is a byproduct of copper. So, for the U.S. to reduce its reliance on unreliable sources of key minerals used in military and renewable technology, greater focus and emphasis should be directed toward the midstream.

[1] Except for REEs which appear to be heavily concentrated in China.

[2] https://montana-aluminum.com/